|

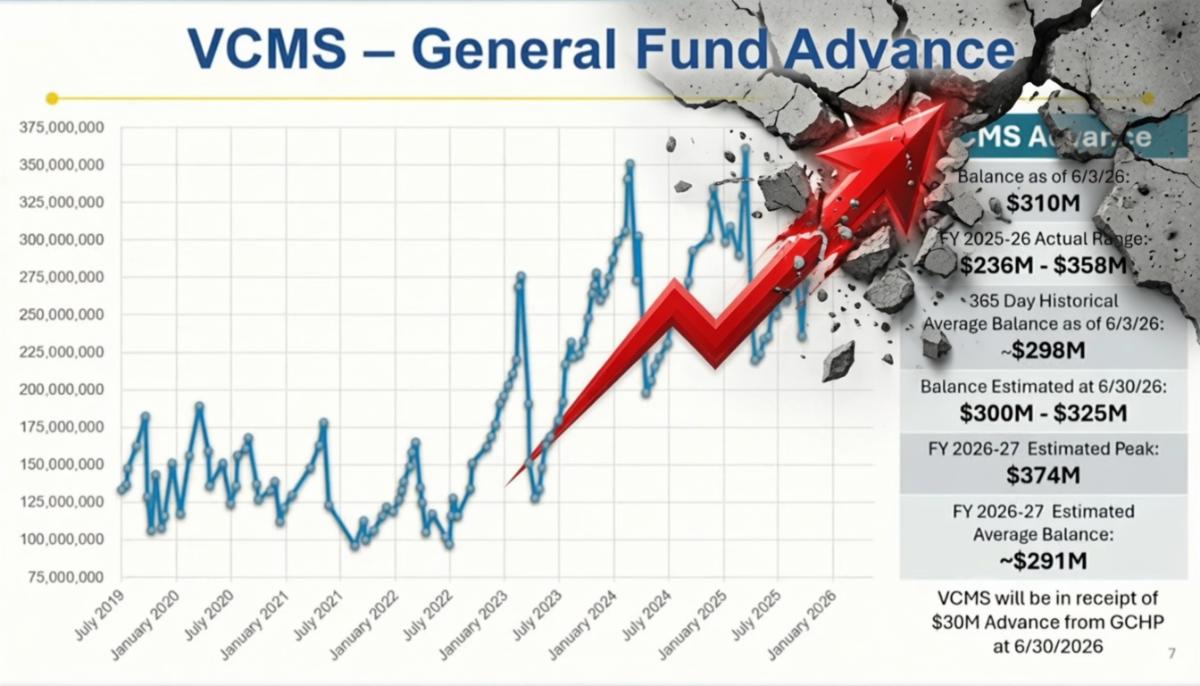

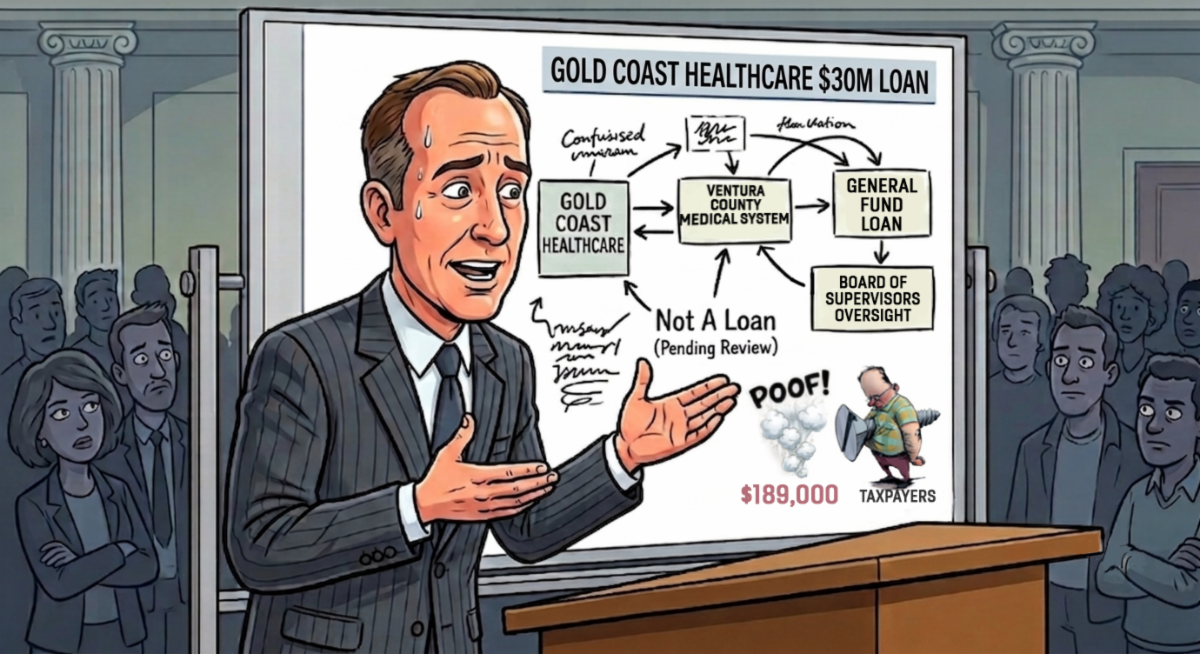

Temporary accounting maneuvers by the Board of Supervisors and senior management do not solve structural financial problems.

Whether this transaction was intended to improve year-end financial reporting or simply provide short-term liquidity, the larger issue remains unchanged: VCMS continues to spend more cash than it generates, and taxpayers continue to finance the difference.

The Ventura County Taxpayers Association supports quality healthcare services for Ventura County residents. However, continued borrowing without a credible repayment strategy is not a financial plan.

Taxpayers can draw their own conclusions. But unless someone can explain why VCMS needed a $30 million outside loan after the Board had already authorized $325 million in General Fund borrowing authority, the transaction appears to have accomplished only one thing:

It temporarily reduced the reported General Fund loan balance at fiscal year-end while costing taxpayers an additional $189,000.

That is why the Ventura County Taxpayers Association continues to ask one simple question:

Why was the Gold Coast loan necessary in the first place? |