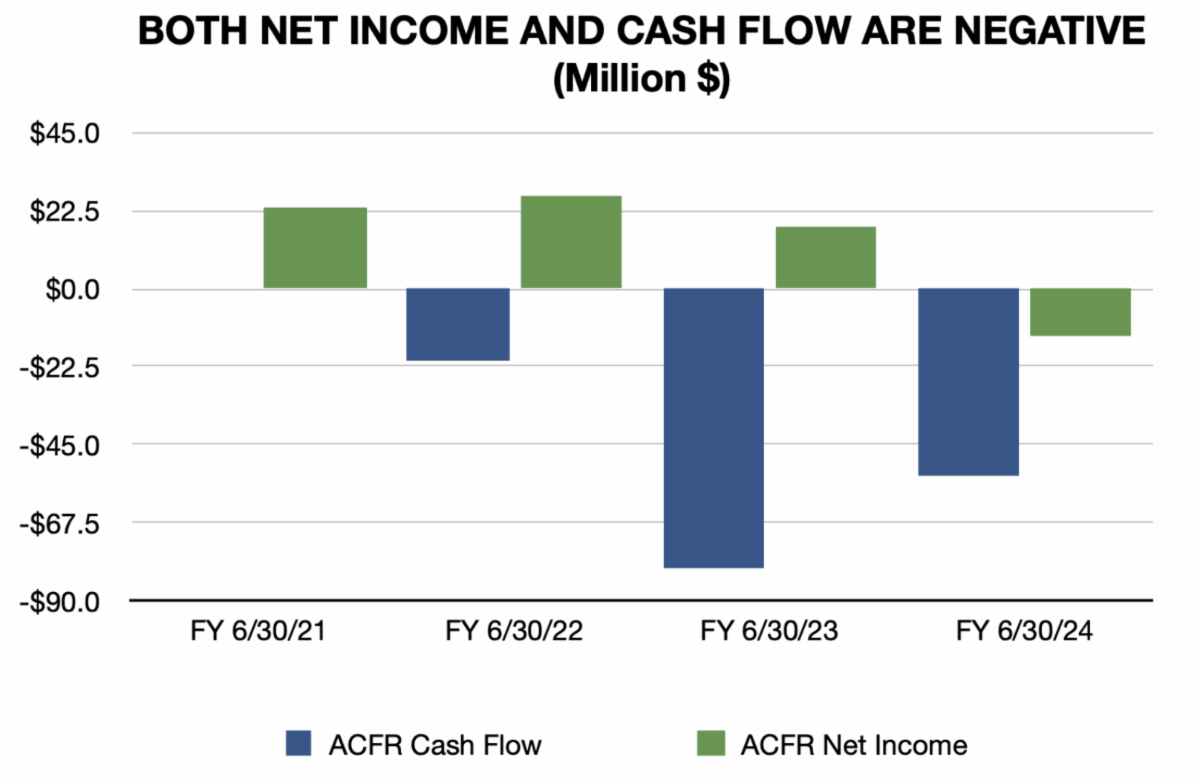

| A Growing Burden on the County General Fund

VCMS is currently operating only because the Board continues authorizing open-ended transfers from the County General Fund. Each new infusion of taxpayer dollars masks the underlying cash-flow crisis while deepening long-term fiscal risk for the County.

County CFO Scott Powers stated, “VCMS has required materially large General Fund cash to sustain its activities … which restricts the County’s ability to move forward with the financing of other capital projects.”

Without structural corrections, these cash-flow losses will continue to drain the General Fund, limit resources for essential countywide services, and push VCMS toward insolvency.

A Pattern of Excuses and Deflection

When faced with questions about worsening finances, VCMS management routinely points to external factors — slow State payments, industry trends, reimbursement delays — anything but the internal cost structure and failure to control spending. This pattern of deflection has prevented meaningful oversight and delayed the hard choices needed to restore financial stability.

A New Distraction: Shifting Focus to HR1

Management has now pivoted to discussing the potential impacts of HR1. While federal policy changes warrant monitoring, raising HR1 as a primary concern before addressing the structural cash-flow deficit is premature and misplaced.

Fix the cash-flow crisis first. Then, evaluate HR1.

Until VCMS eliminates its ongoing structural deficit and restores positive cash flow, every new issue — including HR1 — is secondary. |